Dangers of a Hotchpot Clause in a Will – Re Cosier

Do Equalisation clauses make your Will fair?

We want to treat our children equally. In our Wills, we put in an Equalisation clause. Or we put a Hotchpot clause in our Will. But neither an Equalisation clause nor a Hotchpot clause in Wills works.

A Hotchpot Clause tries to balance and treat the beneficiaries fairly. Hotchpot Clauses date back 100s of years. However, Australians rarely use Hotchpot clauses in Wills.

A ‘Hotchpot’ in an Australian Will:

- is ‘mixture of property’

- it includes not just property in your Will

- it may include property you currently own but may not own in the future

- it may even deal with property that you have never owned

- it may not even deal with property you have never controlled

You can use Hotchpot clauses in both Wills and trusts. They try to ensure fairness for beneficiaries, family members, and loved ones. This is by taking into consideration amounts already received when calculating the final amount due to the beneficiaries under the terms of the trust or Will.

A Hotchpot Clause in a Will equalises the benefits that beneficiaries have already received. You gave gifts only to a few of your children: Re Cosier (1897) 1 Ch. 325 (C.A.).

Equalisation clauses in a Will to make it fair for all children

Example of a Hotchpot Clause to make my Will fair:

- The oldest son already got one of your houses before you died.

- You paid for the wedding of all but one of your children.

- You gave $100,000 to each grandchild, but there are more grandchildren after you die.

- Your ex-spouse gave an asset to only one of the children.

- Your father gave an asset to only one of his grandchildren.

- The son got the farm from a Family Trust.

The judge in Re Cosier stated

‘What is the object of every hotchpot clause? It is simply to prevent a person to whom a testator has left a share of his estate, and who has been advanced in the testator’s lifetime, from obtaining, by the combined effect of the bequest and the advance, more of the testator’s property than he intended the legatee should have.’

Black’s Law Dictionary defines “hotchpot” as:

“The blending and mixing [of] property belonging to different persons, in order to divide it equally.”

Hotchpot Clause and fairness in a Will

For fairness, the Will maker refers to:

- property has already been transferred to only one child and is brought into account by the hotchpot

- a debt owing at death is, in turn, converted into an advancement by way of a loan and brought into account by hotchpot

- refers to past and future gifts and benefits from other people, not just the Will maker going to one child, but not the other

A hotchpot clause adds up all the Will maker’s assets and perhaps assets the Will maker controlled or even did not control. This includes the amounts the beneficiaries already received during the Will maker’s lifetime. This ensures an equal division. This is between the beneficiaries at the will-maker’s death.

Advances to a beneficiary are taken into account at the will-maker’s death. Such beneficiaries’ share under the Will is reduced accordingly. ‘Advances’ are difficult to prove and often impossible to value. They are also subject to CGT, stamp duty and other unknowable death taxes.

Here is an example of a hotchpotch clause that was unfair to everyone: Beatrice McCleary v Metlik Investments Pty Limited, Beatrice McCleary v Benedict Chan; Clement Chan v Benedict Chan [2015] NSWSC 1043, appealed at [2016] NSWCA 222.

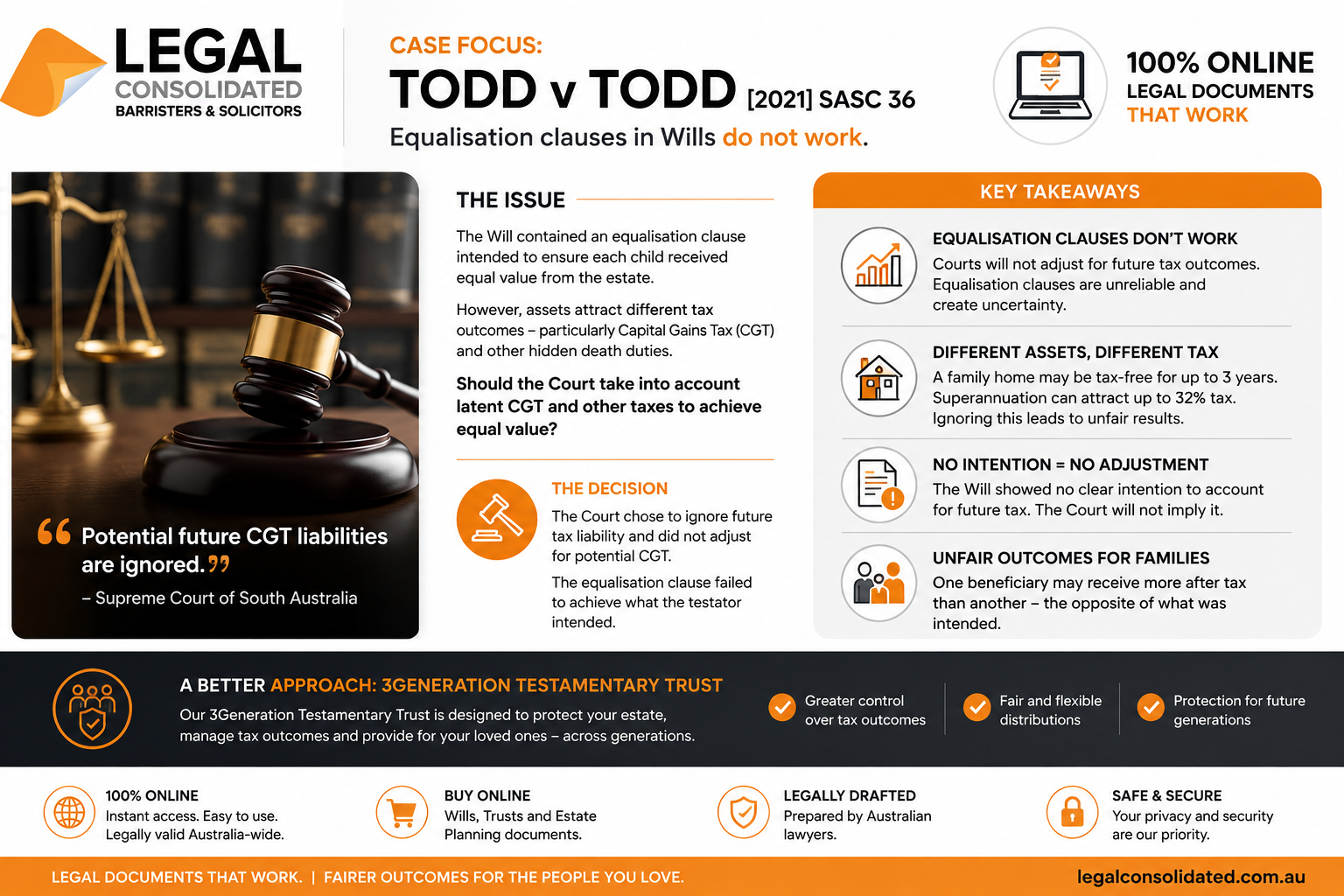

Tax equalisation provisions in Wills do not work – Todd v Todd

Equalisation provisions in Wills usually fail. Consider Todd v Todd [2021] SASC 36.

The Will maker puts in his Will:

“divided between (the beneficiaries) in such a manner so as to ensure that as at the finalisation of the administration of my estate all of my said children have received an equal value of bequests under this my will”.

But assets at death are often pregnant with Capital Gains Tax and other hidden death duties. A family home is often tax-free for up to 3 years from the date of death. In contrast, superannuation suffers up to 32% on death. Should the Court take into account accumulated (latent) CGT liability and other taxes for each asset?

To equalise the deceased estate, do Courts consider potential CGT in our Will? Todd v Todd

Should you consider CGT and the valuation method for an estate asset? It depends on the facts. Every deceased estate is different. You need to consider how likely it is that the beneficiary will sell or otherwise dispose of the asset.

A home in your family for five generations may be kept by the beneficiary. But a balanced share portfolio may be liquidated after the Will maker dies by the beneficiary.

Is the sale of an estate asset inevitable? Then, generally, allowance is made for any CGT payable. The gift under the Will is worth less because the beneficiary has to pay CGT to the ATO when the asset is disposed of.

Sadly, in Todd v Todd, the Court chooses to ignore future tax liability. Potential future CGT liabilities are ignored. In part, this is because the Will evidenced no intention. This is to ascertain the equal value of bequests for future taxation liability.

People on high incomes pay more CGT than people paying tax at a lower marginal tax rate. But is it relevant? Should a rich person be given more of a CGT asset to ‘equalise’ his position?

Craven v Bradley – another example that equalisation clauses in Wills do not work

Look at Craven v Bradley [2021] VSC 344. It shows the confusion of Will equalisation when CGT is considered.

Attempt for estate equalisation in Craven v Bradley to reduce Capital Gains Tax

Dad, in his Will, gifts two properties to two of his three boys.

He then put in an equalisation clause. While the two boys got the property, the third child needs to be ‘topped up’. To make it ‘even’. Bring on the mess.

The equalisation clause wants the children to take into account the different values of the two properties.

Here is the mess of confusion that this poor Will maker contaminated his Will with:

- If the remaining balance is more than 3 times the value of property X, then I give property X to my son A free of all duties and encumbrances, and after all costs associated with its transfer have been met from my estate, and the value of property X is included in the gift to my son A.

- If the remaining balance of my estate is less than 3 times the value of property X, then I give property X to my son A free of all duties and encumbrances, provided he pays to my estate the difference between the value of property X and one-third of the balance of my estate as aforesaid.

- The value of property X should be determined by a registered valuer and on terms that would be granted to an arm’s length purchaser from my estate.

- In relation to one of the properties, the value of the property for the purposes of the will was to be calculated after deducting ‘an amount equal to the capital gains tax liability my estate would pay if the property were sold at the date of my death.

The last bit seems to be an attempt to deal with the capital gains tax on the two properties. One of the properties is the Willmaker’s family home. And that is usually, though not always, CGT-exempt.

How do you equalise CGT in a Will? The problem with equalisation clauses in Wills

The key questions in dispute, and the decision of the court, were:

- is CGT calculated on the will maker’s taxable income?

- or is CGT calculated on the beneficiary’s taxable income?

- or to the estate’s taxable income on the date of the will maker’s death?

- the court held that the estate is the relevant taxpayer – sadly, this is a light approach to the problems of CGT

- it fails to consider what date the value of the main residence is calculated. Is it the date of the will maker’s death? Or the point in time when the son paid into the estate the difference between the value of that property and one-third of the remaining balance of the estate, or the date the property was transferred to the son.

- To add complexity, each State’s laws treat this question differently.

- There is a statutory presumption. This is because the CGT date is the date of the will maker’s death. But this can be rebutted in your Will. And neither Western Australia nor the ACT has this presumption.

- Confronted with this equalisation clause mess, the court states that the statutory presumption is not rebutted. Therefore, the date of death is the date for CGT purposes.

Hotchpotch and equalisation clauses in Wills are like a contract

Interpreting a Will is a bit like interpreting a contract. In Craven v Bradley the court considers the purpose of the Will. What is the purpose of a particular provision? What facts are known and assumed by the will maker? This is at the time the Will is signed. You are applying common sense. You ignore evidence of subjective intention. This was also the approach in Marley v Rawlings [2015] AC 129.

No will is made in a vacuum: Perrin v Morgan [1943] AC 399.

You cannot merely see the Willmaker’s intention in the literal meaning of the words. Consider also the surrounding circumstances. The Court avoids literal interpretations that give rise to absurdities.

Sensible interpretations are better: Re Lapalme; Daley v Leeton [2019] VSC 534.

But if it gives particular meaning to a word, then on the face of it, the Court should adopt that meaning: ANZ Executors & Trustee Co Ltd v McNab (1999) 3 VR 666.

A Court can even insert missing words into the Will. This is if it helps clarify the Willmaker’s intention: Butlin v Butlin [1966] HCA 4.

The Court interprets the Will as a ‘wise and just testator’. Read the Will as a whole. Look to the surrounding circumstances. What if the ordinary meaning of the words in the Will does not make sense? Consider extrinsic evidence under the ‘armchair principle’. The Court considers evidence of the circumstances surrounding the will maker at the time of signing the Will. Consider Re Staughton; Grant v McMillan [2017] VSC 359.

But the Court cannot rewrite a Will merely because it suspects the willmaker did not mean what is said: Perrin v Morgan [1943] AC 399.

As you can see above in Todd v Todd, the court decided that the Will maker in seeking ‘equalisation did not want the future potential taxation liabilities taken into account.

Is the attempt at estate equalisation only approximate? For example, does the son who did not receive a property have to pay the costs of that investment if he wants to obtain a property? Such costs include substantial transfer (stamp) duty. In contrast, the other two boys got their properties free of stamp duty.

What does Craven v Bradley say about Hotchpot and Equalisation Clauses in Wills?

Hotchpot and Equalisation Clauses are too complex to put in a Will. There are better ways to produce fairness among your children.

Other problems of equalisation in Wills

What if a beneficiary is a non-resident for tax purposes?

Hotchpot clauses and attempts at equalisation are a mess. They add ambiguity and complexity to your Will. There are better ways to achieve Estate Equalisation.

Forget about hotchpotch clauses. Can my Will deal with assets I do not own?

Look at Wheatley v Lakshmanan [2022] NSWSC 583.

The Will seeks to gift, unencumbered, a commercial property. There is a further power for the property to “be placed into a trust or superannuation fund of (the child’s) choice”.

But the property is not owned by the Will maker. It is owned by a company. Now, sure, the sole shareholder is the Will makers. But the company, not the Will maker, owns the property. And whoever owns the shares (under the Will) controls all assets in the company. So the shareholder controls the property, not the Will.

Hotchpotch clauses using Specific gift clauses in a Will are problematic

Legal Consolidated dislikes Specific Gifts in Wills. And here is another example of a Specific Gift that fails. The Court confirms:

- A Will only gives away assets that you own, in your own name.

- Confusingly (specific gifts often lead to mess), the Will maker can direct the Executor to do things to ‘reduce into possession an asset not owned by the will maker’. But this does not work. See Re O’Callaghan, [1972] VR 248.

- Make sure the beneficiary receives the company’s shares. (But this is problematic if the company holds other assets or debts.)

The Specific Gift fails – as they often do. But in this instance, the person can challenge the Will.

By challenging the Will, the upset beneficiary gets some cash. But it is nothing like the property’s value. There would have been a lot of tax and stamp duty on getting the money out of a company, as there often is, which would have reduced what they would have got further.

On the bright side, the court noted that the parties had become feral. With the need to win at all costs. Consequently, the accounting and legal fees are very high. So at least the accountants and lawyers got well-fed.

Tanner v Tanner – even a ‘simple’ advancement clause is a disaster

Think a basic clause forcing a child to account for an earlier property transfer is safe? Look at Tanner v Tanner [2026] NSWCA 100. It is an example of how hotchpot and advancement directions invite siblings to sue each other.

Mum wants to be fair. She leaves her estate equally among her three children.

But wait. Years ago, Mum and Dad transferred a block of land to one son and his wife.

Mum puts an ‘advancement’ clause (Clause 5) in her Will. She directs that the son’s share of the estate be reduced by the value of that land. Bring on the mess.

The son goes to the Supreme Court. And when he loses, he drags his siblings to the Court of Appeal. He argues:

-

Mum did not even own the land when she died, so she had no power to make the direction.

-

The old transfer paperwork stated he paid $100,000 for the property. Therefore, it was not a ‘gift’ or an ‘advancement’.

How does the Court interpret Mrs Tanner’s advancement clauses?

The Court of Appeal dismisses the greedy son’s appeal with costs.

The court rules that, based on the construction of the Will, it does not matter if the transfer was a gift or an advancement. It also does not matter that Mum did not own the land at the date of her death. The clause still works to reduce his share.

Further, the court laughs at the son’s argument about the $100,000. The son claimed the transfer document was ‘uncontested evidence’ that he paid for the land. But just because a piece of paper says consideration was received does not make it true. There was zero evidence that the money ever actually changed hands.

Why advancement and hotchpot clauses fail in Australian estate planning: Tanner v Tanner

While the Court ultimately upheld the mother’s clause, look at the damage done. The Will maker’s attempt at ‘fairness’ dragged her three children through two expensive court battles.

Advancement and hotchpot directions force your Executor to act as a forensic accountant. They turn ancient family history, missing bank records, and old property transfers into ammunition for lawsuits. Estate assets are wasted on legal fees, ensuring the lawyers are, once again, well-fed.

Granny flats in your parents’ Will – what is fair?

Mum builds a $450k granny flat in your backyard. Your brother states that when Mum dies, it is not fair that you get the $450k asset for free. Start building a Legal Consolidated Will to address this issue. The granny flat depreciates in value over time. Also, Mum is living on the block without paying for electricity. Or, is she? Best to openly discuss these issues with all the family members.

Can I use a Life estate to achieve equalisation in a Will?

Life estates and Rights to Reside have their own issues, which are explained here.

Protects from death duties, divorcing and bankrupt children and a 32% tax on super. Build online with free lifetime updates:

Couples Bundle

includes 3-Generation Testamentary Trust Wills and 4 POAs

Singles Bundle

includes 3-Generation Testamentary Trust Will and 2 POAs

Death Taxes

- Australia’s four death duties

- 32% tax on superannuation to children

- Selling a dead person’s home tax-free

- HECs debt at death

- CGT on dead wife’s wedding ring

- Extra tax on Charities

Vulnerable children and spend-thrifts

- Your Will includes:

- Divorce Protection Trust if children divorce

- Bankruptcy Trusts

- Special Disability Trust (free vulnerable children in Wills Training Video)

- Guardians for under 18-year-old children

- Considered person clause to stop Will challenges

Second Marriages & Challenging Will

- Contractual Will Agreement for second marriages

- Wills for blended families

- Do Marriages and Divorce revoke my Will?

- Can my lover challenge my Will?

- Make my Will fair: hotchpot clauses v Equalisation?

What if I:

- have assets or beneficiaries overseas?

- lack mental capacity to sign my Will?

- sign my Will in hospital or isolating?

- lose my Will or my home burns down?

- have addresses changed in my Will?

- have nicknames and alias names?

- want free storage of my Wills and POAs?

- put Specific Gifts in Wills

- build my parent’s Wills?

- leave money to my pets?

- want my adviser or accountant to build the Will for me?

Assets not in your Will

- Joint tenancy assets and the family home

- Loans to children, parents or company

- Gifts and forgiving a debt before you die

- Who controls my Company at death?

- Family Trusts:

- Changing control with Backup Appointors

- losing Centrelink and winding up Family Trust

- Does my Family Trust go in my Will?

Power of Attorney

Money POAs: NSW, VIC, QLD, WA, SA, TAS, ACT & NT

Money POAs: NSW, VIC, QLD, WA, SA, TAS, ACT & NT

- be used to steal my money?

- act as trustee of my trust?

- change my Superannuation binding nomination?

- be witnessed by my financial planner witness?

- be signed if I lack mental capacity?

- Medical, Lifestyle, Guardianships, and Care Directives:

- Company POA when directors go missing, insane or die

After death

- Free Wish List to be kept with your Will

- Burial arrangements

- How to amend a Testamentary Trust after you die

- What happens to mortgages when I die?

- Family Court looks at dead Dad’s Will