‘Life Estates’ do not work. Life estates in Wills are bad for tax. A ‘Right to reside’ is no better.

A Life Estate (including under a Will) is an asset with two owners:- Life Tenant – this person has the exclusive right to live and make a profit out of the property until he or she dies.

- right to possess and enjoy the asset and its income until death

- all rights over the asset – but not the right to pass the estate to heirs

- Remainderperson – these people are patiently waiting for the Life Tenant to die. The Remainderperson has no right to be on the property until the Life Tenant dies.

-

- once the life tenant dies, ownership of the asset goes to the ‘remainderperson’

- the remainderperson takes the asset when the Life Estate ends

- remainderperson’s interest is an asset:

-

- you can sell it; and

- you can leave it in your Will

-

- a Remainderperson is also known as:

-

- ‘estate in remainder; or

- ‘remainderman’ (sexist terms are not tolerated at Legal Consolidated, we do not use that outdated expression)

-

How to create a Life Tenancy and Estate in Remainder

- You own a property as a sole proprietor. (It could be any asset, such as a car. But it is usually real estate. And often that real estate is a family home.) The property title deed reads:

- You – sole proprietor

- Like a chocolate bar, you break it in half. You give some of the property to the ‘life tenant’. You give the other bit to the ‘remainder person’:

- The life tenant gets the exclusive right to possess and occupy the property until the life tenant dies.

- You give another person the right to the property. But this is only after the life tenant dies. This person or persons is called the remainderperson. The reminderperson has no right to be on the property until the Life Tenant dies.

- On the title deed:

- Life Tenant – Joanne the second ‘ditzy’ wife

- Remainderperson – Fred and Mavis the aged husband’s children from his first marriage

- When the life tenant dies the:

- life tenancy is ‘extinguished’

- life tenancy disappears as if it never existed

- ‘remainderperson’ gets the property as the sole owner. The title deed now states:

- Owners: Fred and Mavis as sole proprietors

Example of a Life Tenancy

- Old husband Nicholas loves his young wife Delphine. But, being a woman, it is best that she does not own assets in her name.

- Nicholas does not want their family home to go to Delphine when he dies. But he does want her to live in the home until her death.

- Nicholas and Delphine have two beautiful children together: Damon and Helena.

- Nicholas and his wife Delphine both want all assets, including the home, to go to their two children after both of them are dead.

- As you would expect, the family home is solely in old husband Nicholas’s name.

- Husband Nicholas puts this Specific Gift in his Will:

- Asset: 17 Camilla Street, Windella, NSW 2320 (home)

- Life Tenant: his wife Delphine

- Remainderpersons: their children Damon and Helena

- Husband Nicholas dies

- As per the terms of Nicholas’s Will, the home is transferred. The title deeds records:

- Wife Delphine as Life Tenant

- Children Damon and Helena at Remainderpersons

- Surviving wife, Delphine, tries to sell her life tenancy

- Wife Delphine speaks to a real estate agent about selling her Life Tenancy interest in the home. A Life Tenancy is sellable. The potential purchaser could buy her Life Tenancy and live in the home until Delphine dies. But there is a risk for the potential purchaser. Delphine is young. But if she gets knocked over by a bus the day after she sells the Life Tenancy then the potential purchaser paid money to only live in the home for one day!

- Even though the home is worth about $2m, the real estate agent suggests that her Life Tenancy is only worth about $285k. Delphine decides not to try and sell her Life Tenancy.

- After the death of her husband, Delphine moves to Greece. She rents out the home and keeps the rent. Life Tenants are allowed to do this.

- The children, Damon and Helena, try and sell their Remainderperson interest

- The children, Damon and Helena, also approach a real estate agent to sell their Remianderperons’ interest. Remainderpersons are legally able to sell their interest in the property. The interest of a remainderperson is transferred without disturbing the interest of the life tenant. However, the real estate agent states there is a risk for any potential purchaser:

- This is because the Remainderperson gets no access to the home (or rent) until their mother, Delphine (as Life Tenant) dies.

- The potential purchaser hands over money now to buy the Remainderpersons’ interest. But Mum may not die until she is 110 years old.

- The real estate agent states that this is not a common transaction. He has never done this before.

- He estimates the value of the home at about $2m.

- But the Remainderperson’s interest, especially given ‘your mother’s young age’ is $480k. (That would only give each child $240k each).

- The real estate agent muses that mum Delphine and the two children could get together to sell the ‘whole lot’. Then they would get the full $2m between them. The children decline to raise that issue with Mum.

- The son, Damon goes Bankrupt

- Damon, the son, enters into a bad business deal. He goes bankrupt.

- There was no bankruptcy trust in his Dad’s Will. (Silly dead Nicholashe should have built a 3-Generation Testamentary Trust Will.)

- Mr Trustee-in-Bankruptcy gets all of Damon’s assets.

- An interest as a Remainderperson is an asset.

- Mr Trustee-in-Bankruptcy transfers the son’s interest in the home to himself.

- Mr Trustee-in-Bankruptcy is registered on the title as holding a half interest as Remainderperson in the home.

- This is of no concern to Mum or her daughter Helena.

- Mum’s Life Tenancy is unaffected. Daughter Helena’s half interest as a Remainderperson remains the same.

- The Title Deed now states:

- Delphine (Mum) as Life Tenant.

- Mr Trustee-in-Bankruptcy and Helena (daughter) as Remainderpersons.

- Mr Trustee-in-Bankruptcy has never seen a Life Tenancy before. They are rare. Mr Trustee-in-Bankruptcy speaks with his lawyer: “Can’t we force the Mother and Daughter to sell”:

- His lawyer states that the Mother and Daughter cannot be forced to do anything.

- Angry Mr Trustee-in-Bankruptcy sells his half interest in the Remainderperson position for a ‘miserable’ $80k.

- The purchaser of that interest is the mother, Delphine. This is through a Bare Trust Deed so that Mr Trustee-in-Bankruptcy had no idea who the beneficial owner was. This is legal.

- Wife Delphine is a lot smarter than her husband thought!

- The Title Deed to the home now looks like this:

- Delphine (mum) as Life Tenant.

- Delphine (mum) and Helena (daughter) as Remainderpersons.

- Daughter Helena gets divorced

- Helena, the daughter, suffers a divorce.

- Helena keeps her superannuation. However, the family court requires her to transfer all other assets to her ex-husband.

- Silly old Dad, Nicholas, forgot to put a Divorce Protection Trust in his Will. So his daughter Helena’s Remainderperson interest is lost to Helena’s ex-husband.

- The ex-husband gets Helena’s half interest in the Remainderperson.

- The Title Deeds to the home now states

- Delphine – Life Tenant.

- Delphine and Helena’s Ex-Husband – Remainderpersons.

- The ex-husband is furious with this ‘useless’ half Remainderperson interest. What can he do with it? He has to wait until his ex-mother-in-law dies. A happy thought. But ‘it could take decades’.

- The ex-husband values his half interest in the Remainderperson at about $80k. But after 3 months on the market, there are no offers.

- Eventually, there is an offer of $30k from a stranger. The ex-husband takes the money in disgust.

- Yes, you guessed it. Mum has done another Bare Trust. This hides her identity as the potential purchaser.

- The Title Deed to the home now states:

- Delphine as Life Tenant.

- Delphine as Remainderpersons.

- What happens when the life tenant gets the estate in remainder? (Or, what happens when the remainder person gets the life estate?) The life tenancy and the remainder person merge. You end up with just the sole proprietor. The proprietor can update the title deeds. This shows the proprietor as the sole owner: sole proprietor. The life estate and estate-in-remainder are removed. The Title Deed now states:

- Delphine as sole proprietor.

- Yes. Delphine now has a 100% interest in the whole home. It is worth $2m. She sells it for $2m. Good on your Delphine!

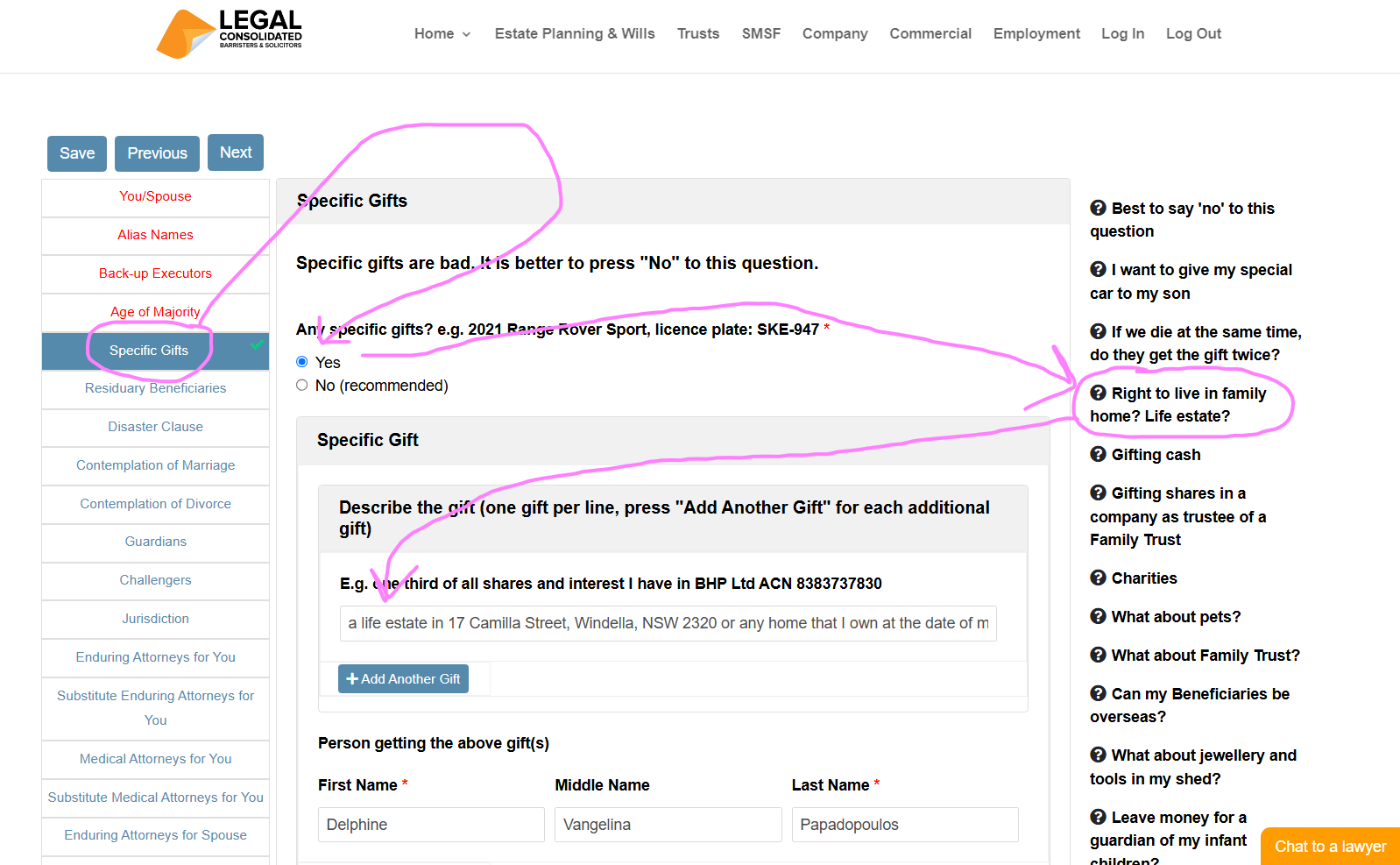

Old husband Nicholas built his Will on LegalConsolidated’s website. He wanted to include a Life Estate for his young wife, Delphine. Here is how he did it:

He built a single 3-Generation Testamentary Trust Will, choosing not to use mirror Wills, as he was not leaving everything to his wife.

When prompted about Specific Gifts, he selected ‘yes’.

He read the provided hints on Life Estates and copied the appropriate wording into his Will.

Under a Legal Consolidated Will, it’s unnecessary to name Remainderpersons separately if they are the recipients of the Residual Estate.

In his Will, Nicholas leaves everything to his two children, except for the Specific Gift of the home, which forms part of the Life Estate for Delphine.

Life estates are created either while you are alive or in your Will when you are dead:

- during your lifetime; or

- in your Will – in Australia, most Life Estates are created in Wills

How does an Australian ‘life estate’ end?

- A Life Estate ends automatically. This is when the life tenant dies.

- Alternatively, if the life tenant and remainderperson agree, they can either sell the asset to a third party or to each other.

Death Taxes on Life Estates and Rights to Reside – TD 2026/D1

There are four de facto death duties in Australia. With Draft Determination TD 2026/D1, the ATO has introduced a new death tax on your family home if it has a right to reside or a life tenancy over it.

But here is the good news: if you have a 3-Generation Testamentary Trust, you are already ahead of the game. Our testamentary trusts are discretionary. This means if a certain asset—like the family home—would benefit by not being in a Testamentary Trust, then it can be left out. That is a decision that the Beneficiaries decide after you are dead.

If you have a 3-Generation Testamentary Trust, you are protected. But if you have a ‘Life Estate’ or ‘Right to Reside,’ then your Will is a ticking time bomb.

Flexibility is the key ingredient to put into your Will to defeat TD 2026/D1

If you have to narrow estate planning down to one word, it is flexibility. This is because of the three great unknowns:

1. You do not know your date of death

2. You do not know what the laws will be

3. You do not know that the assets that you will own at the date of your death (this is the biggest delusion that clients have)

To overcome those great uncertainties, you need flexibility in your Will. The 3-Generation Testamentary Trust is the most flexible structure you can put in your Will. For example, a 3-Generation Testamentary Trust Will does not force you to put an asset inside the trust. The asset, instead, can be transferred directly to the beneficiary. That is a decision that the beneficiary will make after you are dead.

How a 3-Generation Testamentary Trust in your Will works:

-

The beneficiary has the discretion to choose which assets go into the testamentary trust.

-

For example, for the family home, the beneficiary may choose to inherit it personally.

-

This preserves the Two-Year Rule (sometimes three). They can sell the home 100% tax-free within two (or three) years of your death.

Review your Will if it contains a life estate or right to reside

Coming back to the ATO’s TD 2026/D1, it targets Life Estates and Rights to Reside. We have been trying to talk clients out of putting specific gifts in Wills, such as life estates, since 1988. So very few of our clients have life estates or rights to reside in their Wills.

However, if you do have either in your Will, then it needs to be reviewed. All Legal Consolidated Wills and POAs can be reviewed as often as you wish, free of charge. Just email us a high-quality colour scan of the Legal Consolidated Will to lawyer@legalconsolidated.com.au

How to remove life estates and rights to reside from your Will for free

Laws change. The ATO changes its mind. Your family circumstances change. A Will should not be a static document gathering dust.

This is why all our 3-Generation Testamentary Trust Wills come with free updates for life.

-

You can update your Will on our website as often as you wish.

-

There is no cost.

-

If you separate, divorce, or if the ATO introduces a new death tax, such as TD 2026/D1, you can update your Wills for free.

Young and Vulnerable Children tool kit

Free resources to help protect young and vulnerable children:- Vulnerable children in Wills – watch the training course

- Loans to children – in case they divorce or go bankrupt

- Divorce Protection Trusts in Wills – in case a beneficiary, child or grandchild separates

- Making Wills for your children

- Special Disability Trusts – for disabled children

- Elder Abuse – protecting the children as well

- Child renounces a gift or Family Trust distribution for Centrelink and stop Trustee-in-Bankruptcy

- Children paying 32% on your super when you die

- Only disabled children can take your SMSF Reversionary Pension

- A parent dies child pays 66% tax

- Dad’s Will: child vs charity

- Son loses the farm to his two greedy sisters

- Disabled dad has $9m, two children and no Will

- Court rewrites disabled Dad’s Will to protect children

Life Estates in an Australian Will

Life estates in a Will are silly and old-fashioned. You should instead leave everything as a percentage. If you want to benefit one particular person then increase their percentage. Therefore, your Residuary Beneficiaries work out what they want to do with your estate. Life estates are just a prison sentence. Life estates are commonly put in place by people who want to rule from the grave. That is a dangerous practice.1. Stay-at-home child gets a life estate

Young Jonny looked after his ageing mum. His siblings selfishly got married, had children and lived a life. So Jonny gets a special reward. After Mum’s death, she allows Jonny to live in the family home until he dies. Sweet as that all sounds, that is a mess and a recipe for disaster:- Before death, Mum suffered a stroke. She has been moved into a nursing home. Mum is of unsound mind, and the government/children sell the family home. It now attracts Capital Gains Tax and Land Tax. Poor Jonny misses out.

- Or, at Mum’s death, Jonny is now stuck in the house. Jonny wants to see the world and get a life – but he has no money. He just has an old house to wander around in. Perhaps Jonny wants to get a smaller, newer apartment. He cannot. He is trapped in a large, ageing house that no one has any interest in maintaining.

2. Hot toy boy gets a life estate

82-year-old Mavis finds a 48-year-old toyboy at her Bridge Club. He is not bright. He is not wealthy. But he is a lot of fun and as handsome as sin. Mavis, in her Will, gives a life estate to this young fellow. Maybe they got married, maybe they just lived together. It makes no difference. Mavis dies. The toy boy is now stuck in a big house. He cannot sell it. He cannot maintain it. And then he suffers a stroke and moves into a cheap retirement home because he has no money. The house is left derelict. Instead, Mavis should have left a percentage of her estate to the toy boy. He is then free to use the money to enjoy his life.The Life Estate: A ‘Virtual Cage’ built by a dead hand

A Will is not a tool for posthumous control. Its legal and moral function is to get rid of what you own and, where relevant, to provide for the proper maintenance and support of those you leave behind. A life estate, particularly over the family home, often fails this fundamental test. While perhaps well-intentioned, it is an archaic and clumsy device that frequently becomes what we call a “virtual cage” for the surviving partner. Cage A matter our firm handled illustrates the impracticality and inherent cruelty of shackling a beneficiary to a property. The situation raised the critical legal question of what constitutes ‘adequate provision’ under family provision legislation across the states, such as Chapter 3 of the Succession Act 2006 (New South Wales). Our client was a 74-year-old widow. Her late husband’s Will had left her a life interest in their large family home, an asset that was now too big, too expensive to maintain, and wholly unsuitable for her needs. The Will effectively trapped her. She couldn’t sell the house to move to a more manageable home or to fund a bond for an aged care facility. She was asset-rich but cash-poor, burdened by a property she could no longer manage. Had the matter proceeded to a final court hearing, a judge would likely have dismantled the life estate. The court’s role is pragmatic. Forcing a widow to remain in an unsuitable home ignores the realities of ageing. A mere right to occupy is not a genuine financial provision. Proper maintenance requires the flexibility to address future needs, such as moving to a smaller home or a care facility. A core failure of a life estate is its rigidity. It strips the beneficiary of autonomy and the security that comes with having a negotiable asset. A person’s financial security should not be chained to a single, illiquid asset. Instead, they need a measure of independence to meet life’s challenges as they age. Such limited interests often fail to provide the financial security and independence that a surviving spouse requires. The lesson from these matters is brutal and clear: do not mistake a life estate for a gift. It is a restriction. It is the dead hand of the Will maker reaching out to control a beneficiary from the grave, preventing them from making their own decisions as their life circumstances change. It is, in effect, a cage. Providing the capital, whether through a lump sum or the asset itself, is a far better way to ensure true independence and make adequate provision.Do you still want a life estate or right to reside in your Will?

Not convinced? Start building a 3-Generation Testamentary Trust Will on our website. For free see the wording to put in your Will for:- Life Estate

- Right to Reside (also called a Right to Occupy)

Gifting Life Estates in Wills

Can I gift a life estate in my Will?

You cannot put your life estate in your Will. This is because your life estate dies when you die. Your Will only begins to operate when you are dead.

So, by very definition, a Life Tenant cannot gift their life tenancy in their Will.

Can a Remainder person leave their interest in their Will?

A Remainderperson can leave their remainder person interest in their Will. Upon their death, the remainder interest goes to the beneficiaries named in the Will. Just as the Remainderperson cannot access the property so the beneficiaries cannot enter the property. The Life Tenant must die first.

The difference between a Right to Reside and a Life Estate Tenancy

A ‘right to reside’ is different from a ‘life tenancy’. A Right to Reside is delicate. A life tenant has the right to move out of the home and rent it out. But if a person holding a Right to Reside vacates the home, then the Right to Reside is lost. Another name for a ‘right to reside’ is ‘right to occupy’.‘Right to reside’ cannot be sold

As you can see above, a Life Tenancy can be sold. But a Right to Reside cannot be sold. The:

As you can see above, a Life Tenancy can be sold. But a Right to Reside cannot be sold. The:

- toy boy

- stay-at-home child

- second wife

- other unlucky people

A Right to Reside is also known as a Right of Residence.

A right to reside is when you give your loved one (beneficiary) the right to live in your property. This is often a specific gift in our Will. Yes, this sounds very much like a ‘life tenancy’. But they are different. A life estate is a right to possession of the property for life. A life estate is robust. A life tenancy can be sold.Right to reside is lost when you move out of the property

In contrast, the right to reside can also be for the life of the beneficiary. Or it can be for a limited time. For example, 24 months from the date of your death. It can also be until a certain event happens, for example, the beneficiary stops living in the property.Both the ‘life tenancy’ and ‘right to reside’ have responsibilities:

- maintaining the property

- paying property expenses

Life estates are registered on the title deeds. The right to reside is just a caveat

In Australia, you cannot register ‘trusts’ on the front page of the properties’ title deed. But a ‘life tenancy’ is not a trust. The life tenancy interest is registered on the front page of the title deed. The life tenancy interest is registered as a ‘proprietor’ of the property. In contrast, the weaker ‘right to reside’ is registered under a caveat on the back page of the title deeds.Adverse taxation of life estates

Life estates are riddled with tax uncertainty. There are two conflicting views on what occurs when a life interest is granted:- Did the grant create a new asset?

- Or is the grant of such an estate a part disposal of an existing asset?

ATO’s position on life estates: PS LA 2003/12

The ATO’s PS LA 2003/12 is relevant to the ending of a life tenancy. This is if the trustee has the power to distribute assets in a testamentary trust to end the life tenant’s interest. What happens when the life tenant dies and the asset goes to the remainderperson? PS LA 2003/12 states that the remainderperson gets the CGT section 128-15(3) exemption.ATO TR 2006/14 – transferring a life estate

In contrast, what happens if the life tenant gives up the life tenancy while still alive? What are the tax consequences of terminating prematurely a life interest? TR 2006/14? The trustee is treated as the relevant asset ‘owner’. The trustee’s cost base is the cost base of the asset in the dead person’s hands. Or, if it was a pre-CGT asset, its market value at the date of death (see paragraph 18). What about the beneficiaries? They also each have separate CGT assets. These are their ‘trust interests – the equitable life and remainder interests’ (see paragraphs 24 and 188). The beneficiaries’ interests in the testamentary trust have a cost base equal to their market value (see paragraphs 26 and 144).Value life estate and remainderperson’s interests to find the cost bases?

Are the assets that originally formed part of the deceased’s estate exempt from CGT? Yes. But only if they pass from the executor to the remainderperson. This is under the terms of the Will (paragraph 45). This repeats in PS LA 2003/12. Thankfully, the ruling states that the life tenant does not make a capital gain. This is when they die. See paragraphs 43 and 44. I would have thought this obvious.Tax when a life tenant surrenders their life estate interest

Life interests imply until the life tenant finally dies. But the life tenant may wish to surrender the life interest earlier. This may be for free or for a price. Either way, this is a ‘disposal’ under the CGT regime. This is a different situation from getting something in a Will. Gifts in Will carry CGT relief, especially if your Will contains a 3-Generation Testamentary Trust. Consider:- whether the property is sold by the trustee or is transferred in specie to the remainder beneficiaries; and

- whether there are multiple remainder beneficiaries or whether there is a sole remainder beneficiary

For tax purposes, a life estate is three assets

The Life Tenant has:

* exclusive use of the property

* can sell the life tenancy

* can rent out the property.

The Remainderpersons can not enter until the Life Tenant is dead.

- the life interest owned by the life tenant

- the deceased’s property that is subject to the life interest and owned by the trustee (“deceased’s property”); and

- the remainder interest owned by the remainder beneficiaries

Remainderpersons don’t get the ‘principal place of residence exemption’

What if the ATO successfully argued that an early release by the life tenant was not in the terms of the Will? Then the executor realises a capital gain under CGT event E5 or E7. Both the ATO and I agree that this approach applies in dealings between the life tenant and the remainderperson. This is where the life tenant gets payment for relinquishing the share or part of the proceeds of the sale. But I would think the ATO is wrong to invoke CGT if there was merely an early surrender by the life tenant. Other issues are calculating the cost base and the loss of the principal place of residence exemption. For example, your mum and dad die. Your alcoholic brother gets a life estate. You get the remainderperson interest. Your brother is young. The property is worth $1m. The actuary gives your alcoholic brother a cost base of $700k. Your cost base is $300k. A year later your brother dies of alcoholic poisoning. You are deemed to have acquired the $1m property for $300k. There is no principal place of residence exemption. You sell the property for $1m. You have made a $700k capital gain to put into your tax return. Life estates are bad because they do not work and suffer harsh tax treatment. Life estates are best avoided in your Will. But you may be able to overcome this under section 118-195 Income Tax Assessment Act 1997 (Cth).Wilson v Chapman – life estate linked to ‘income and profit’

In Wilson & Anor v Chapman [2012] QSC 395, the court debated the terminology of life estates. The case was about a Will that gave a life tenant an entitlement to the ‘income and profits’ of trust assets.The facts of Wilson v Chapman – a taxation problem?

- A beneficiary is a life tenant of a trust under a Will,

- The beneficiary is entitled to the ‘income and profits’ from the trust’s assets.

- But what do ‘income’ and ‘profits’ mean? Do you use an ATO definition, common law, or a dictionary definition?

- The court interpreted ‘profits’ to suggest that the willmaker intended the beneficiary to receive more than just income, prompting a look at whether both realised and unrealised capital gains were included in this term.

- The court found that ‘profits’ encompassed net income and net realised capital gains but excluded unrealised capital gains, because, for tax purposes, a realised capital gain is treated as income.

Life Estates and Right to occupy – four additional problems

When drafting and administering life interest trust,s consider:- who pays the expenses and outgoings?

- the risk of family provision claims – a life tenant may still challenge your Will to seek the removal of the life estate

- providing for substitute accommodation – this is just a ghastly mess. Your children want their step-parent to live in a tent on a big block of land (to maximise capital gain). And the stepparent wants to live in a snazzy apartment – with little capital appreciation

- the choice of trustee of a life interest trust – who are the executors?

Life Tenant challenging your Will. “Portable” live estates.

For maximum capital growth, the children of the first marriage want the second wife to live in a tent on a valuable piece of real estate. However, second wife, does not care about capital growth. Instead she wants to live in a penthouse apartment and then a nursing home. Apartments and nursing homes have less capital growth. A family provision claim is when your surviving spouse believes they have not been properly provided for in your Will. They are for second marriages. Your surviving spouse must demonstrate specific elements to the Court to justify an adjustment in their favour. This process involves assessing whether adequate provision can be made from the estate’s assets. The Court often faces a challenge in balancing adequate provision for your second spouse with the rights of your first children and your right to testamentary freedom. This right allows you to distribute your assets in your Will as they see fit. The increasing use of a “Crisp Order” illustrates how the Court sometimes addresses these competing interests. This type of order provides a way to support a claimant without significantly impacting other beneficiaries. A Crisp order gets its name from the decision of Holland J in Crisp v Burns Philp Trustee Co Ltd (18 December 1979, unreported). Ipp JA in Milillo v Konnecke [2009] NSWCA, [47]-[48] explains:“… a Crisp order may entitle a plaintiff, from time to time, to require the executor of a will to sell a home devised by the will, or otherwise owned by the estate, and to use the proceeds for purposes that may include purchasing another home for the plaintiff’s use and occupation, or providing accommodation for the plaintiff in a retirement village or similar institution, or in like accommodation providing hospitalisation and nursing care.

The flexibility provided by such an order underlies the notion that a Crisp order confers a ‘portable life interest’.”

Life Estates and Granny Flats

Another Specific Gift in a Will is a life estate of a granny flat. This is where:- the Will maker gives a right to reside or a life estate in a part of a property to a beneficiary

- that part of the property is where the granny flat is situated

- when the beneficiary dies the right to reside or life estate interests dies with them.

The granny flat life estate is not necessarily for your last to die aged parent.

It is also for your:- first divorced wife, where the property settlement went wrong; or

- 30-year-old child not ready to leave home.

Tax implications of a granny flat life estate

Since 1988, these are the tax issues of granny flat life estates faced by our law firm:- Any payment of money for the right to occupy a granny flat is a capital gains tax (CGT) event. This is event: CGT Event D1.

- CGT Event D1 is triggered even if the granny flat is created from part of the family home.

- The CGT is payable on the consideration paid for the grant of the granny flat right to occupy. It does not matter if the agreement was verbal or in writing.

- What if the consideration paid is less than the market value? The market value substitution rule applies. The government values the transfer and (stamp) duty and CGT applies.

- There is a risk that the owner of the rest of the property loses, at least in part, the CGT main residence exemption.

1. Bankruptcy and Life Estates

A ‘life interest’ is an asset. It potentially makes income. What happens when the life tenant goes bankrupt? The trustee-in-bankruptcy kicks you out. He takes possession of the asset. He:- leases out your property; and

- can sell the ‘asset’. (Sale of the Life Estate, of course, does not affect the rights of the patient Remainderpersons)

2. Bankruptcy and Right to Occupy

However, what if you only have instead a ‘right to occupy’? A ‘right to occupy’ is an asset. And if you are bankrupt, assets must be put under the control of the trustee-in-bankruptcy. This is for the benefit of your creditors. But you cannot be forced out of your home. Well, to put it another way, if you were forced out of your home, then your ‘right to occupy’ is extinguished. The asset is destroyed. This is by you failed to live in the property. This is a condition and delicate nature of a ‘right to occupy’. But, what if the trustee-in-bankruptcy allows you to remain in the property under the ‘right to reside’. And then deems you to be receiving value or income. This is because you live in the property under a ‘right to occupy’? The Bankruptcy Act 1966 (Cth) defines the concept of ‘income’ widely. The free use of a home may be considered ‘income’.How does Centrelink treat life estates?

Life Interests according to Centrelink

For Centrelink, a life interest represents the right to use or benefit from an asset during an individual’s lifetime but is not part of a trust. Under the Social Security Act (SSAct), a life interest is typically exempt from asset assessment. This is unless there is a specific exception. Notably, if a life interest is established under a Will that also creates a testamentary trust, it remains a personal asset, not an asset of the trust.

Remainderpersons interests according to Centrelink

Centrelink calls a Remainder person’s interest a ‘remainder interest’. For Centrelink, a remainder interest arises when a life interest is created, signifying the residual right to an asset after the life interest ends (ie, this is usually when the life tenant dies). Generally exempt from asset assessment, remainder interests can sometimes exist outside of a trust structure, assessed under general social security rules.

Examples of how Centrelink treats life estates

-

- If a Will creates a life interest and assigns the remainder interest directly to another party without forming a trust, both interests are considered saleable assets held individually by the beneficiaries.

- Conversely, if the Will stipulates that the remainder interest only vests after the life tenant’s death and is part of a trust, it is assessed as an asset of the trust.

How does Centrelink treat a life estate for means testing?

-

- Valuation and Attribution: For remainder interests within trusts, the value is often determined actuarially and may be attributed to the trust controller for tax purposes, potentially affecting eligibility for income support.

- Exemptions and Concessions: Special rules apply for trusts established before 31 March 2001, where the trust’s remainder interest is not attributed to the controller, allowing for financial rearrangement without immediate tax repercussions.

Centrelink provides guidelines that help illustrate the potential complexities involved when using life estates. By attempting to provide for a second spouse while also considering children from a first marriage, well-intentioned estate plans inadvertently create significant logistical and emotional challenges. These situations can lead to conflict and hardship among family members, despite the original aim to support loved ones.

Ruling from the grave – life estate

Q: My partner died suddenly. He left me a ‘life interest’ in our $2m home that we shared together. Two conditions:- I maintain the property and pay the rates, which is fine; and

- I forfeit the life estate if I remarry!

Life Tenant – Joanne has the exclusive right to live in and profit from the home until she dies. You can even sell your life interest. But it is not worth much. Who wants to buy something that ceases to exist when you die? I hope not, but you could die tomorrow.

Remainderperson – the 3 adult children are patiently waiting for you, the Life Tenant, to die. They have no right to be on your property until you die. They can also sell their interest now. But it is not worth much. Because, Lesley, you may live to 120! And I hope you do.

From a Capital Gains Tax perspective, it is a disaster for his three children. The children usually end up with a bigger Capital Gains Tax once they are dead, and they sell the property. Under complex tax laws, the children may be deemed to have acquired the property for say $200,000. If they sell it for $2m, they are up for $180,000 CGT tax. The condition that you lose your Life Estate if you remarry is void. It does not operate. This is because it is contrary to the rule of Public Policy. A Will maker cannot put conditions into the Will, such as the ‘gift is lost if you challenge the Will’ or ‘you lose the gift if you marry a Methodist’. You may wish to challenge the Will and ask that you get the home outright. That ‘no marry’ clause will not make the judge happy. And increases your chance of winning. It also smacks of a homemade Will or post office Will. And they are also easier to challenge. Or, given that the home is worth say $2m, you may wish to, together with the 3 children, sell the home and split the money $1m to you, and $1m between them.See also:

- What happens to super if you go bankrupt?

- How to protect yourself from bankruptcy

- Bankruptcy Trusts in Wills

- Who can challenge your Will?

- CGT on the dead wife’s wedding ring

- Even a pre-1985 family home can be subject to CGT

- Two years to sell your dead parent’s family home exemption – now you can get 3 year