Your children-in-law know you have money

Your child’s spouse knows your family has money.

They wait. They tolerate the marriage a little longer. You die. Your child receives the inheritance. Then the separation starts.

Without protection in your Will, your estate assets are available for Family Court scrutiny. They are in your child’s exposed personal name. The Family Court sees them. The spouse sees them. The fight begins. A Divorce Protection Trust in your Will helps stop that.

Legal Consolidated’s 3-Generation Testamentary Trust Will includes Divorce Protection Trust machinery. It helps keep your estate assets away from your child’s matrimonial dispute. It gives your family control levers. It stops a direct inheritance from becoming litigation bait.

Press START FOR FREE. Read the hints. Watch the training videos. Telephone Legal Consolidated to discuss your answers.

A Divorce Protection Trust works with your 3-Generation Testamentary Trust Will

When you build your tax-effective 3-Generation Testamentary Trust Will on our website, your Will includes protective machinery for divorce, bankruptcy, de facto death duties, vulnerable beneficiaries and superannuation.

How does a Divorce Protection Trust in a Will protect an inheritance?

How does a Divorce Protection Trust in a Will protect an inheritance?

The Divorce Protection Trust delays or stops capital and income going to the beneficiary who is suffering a divorce or separation. It reduces the opportunity for the Family Court to get its hands on the money from your Will.

The Family Law Act gives the Family Court wide powers. In some cases, those powers reach third parties, including executors and trustees.

In a divorce, the Family Court examines how the assets came into the trust. It considers who gave the money to the trust in the first place.

1. If assets come from one of the couples during the relationship and are then put into a trust, the assets are considered part of the marriage. The Court is free to order the transfer of the assets to your child’s ex-spouse.

2. However, this may not apply where the money comes via a Will. Instead of your divorcing child putting money into a trust, you are the one putting the money into the trust (via a Divorce Protection Trust). It is arguably different when the person’s parents gift their assets into a Divorce Protection Trust.

The Family Court can disregard trusts set up to limit its reach as a sham. However, that primarily concerns one of the separating couples taking their money and trying to hide it in a trust. This is not the case here. This money is not from one of the separated couples. Rather, the money is from the parents of one of the separated couples. The money is from an inheritance of a parent, grandparent or great-grandparent. The Divorce Protection Trust is designed so that the inheritance never becomes an asset of the marriage. It is designed to be a trust for the benefit of many beneficiaries, not just the separating person.

Why Divorce Protection Trusts are harder for the Family Court to attack

A Divorce Protection Trust is one of the many types of Testamentary Trusts we put in your Will. There are not many cases on Testamentary Trusts. However, in our experience, the Family Court is less likely to break open a trust in a Will and less likely to plunder testamentary Trusts. The Divorce Protection Trust provides additional safeguards against escaping the Family Court. This is over, and above all the other types of trusts, we put in your 3-Generation Testamentary Trust Will.

Divorce Protection Trust case study: Dad dies, son divorces 3 years later — Bernard v Bernard

In Bernard v Bernard [2019] FamCA 421, the husband and wife married in 1988. They separated in 2015. They divorced in 2017. In 2012, the husband’s father died. He leaves his estate equally to the husband and the husband’s sister. This is under two discretionary testamentary trusts. The husband is the trustee of his sister’s trust. His sister is the trustee of his trust.

Each is the primary beneficiary of their own trust. Each trust has many potential beneficiaries. These include the spouse, children and grandchildren of the primary beneficiary. The facts are:

- Dad dies.

- The son uses the Divorce Protection Trust in the dead Dad’s Will.

- Three years later, the son divorces.

Divorce Protection Trust saves the day in Bernard v Bernard:

The facts of Bernard v Bernard:

- Divorce Protection Trust: set up in Dad’s Will

- Divorce Protection Trust name: they used the divorcing son’s name (pretty irrelevant, I know, but the Family Court is psychological warfare)

- Primary Beneficiary: divorcing son

- Appointor: friendly third party (often, another child, friend, the accountant or financial adviser)

- Trustee: divorcing son’s loving sister

- Beneficiaries: the usual suspects, including the divorcing son, his children, spouses (including the divorcing wife), distant relatives, charities, etc…

Wife tries to defeat the Divorce Protection Trust in the Bernard Will

The wife argues that:

- The divorce protection trusts mirror each other.

- The husband and his sister have the same rights and obligations as trustees of each other’s divorce protection trust.

- They use the two trusts to operate a partnership.

- The husband controls his own trust, as does the sister.

- The husband controlled his own trust, and this control equated to ‘property of the marriage’.

- The wife argues:

‘The reality is the husband and his sister operate their business as a partnership and that their trusts are mirrors of each other [with both] having effective control of the assets in their trusts and therefore those assets are matrimonial property of the husband’.

-

- In paragraph 81, the Judge states that the

‘facts do not support such a finding’.

Bernard v Bernard decision: Divorce Protection Trust not in the matrimonial pool

The Court held that the Divorce Protection Trust was not part of the matrimonial pool. The divorcing wife could not touch the assets. This is because:

- Settlor (Will-maker): was dead dad, not the divorcing son.

- The trusts were established from the assets of the late father’s estate, not from property acquired by the husband before or during his marriage to the wife. The court states in paragraph 66:

‘… the husband does not have legal title to any asset of the trust, nor does he have any power to appoint a trustee or appoint the assets of the fund to a beneficiary. He is a mere beneficiary, albeit described as a primary beneficiary. The husband is dependent upon the trustee of his trust to distribute income, accumulate income, and the trustee has complete discretion in determining any distributions made by the trust.’

- Trustee: was the sister, not the divorcing son

- Appointor: was not the son

- Power and control: remained solely with the Appointor and Trustee (the sister). The husband is a mere beneficiary of his trust. He had no more than a right to due administration and consideration. He has no control over his sister to procure a distribution or appointment of the trust’s assets in his favour. As the trustee, his sister owed fiduciary obligations to all beneficiaries, not just her brother. In paragraph 96, the Court quotes Harris v Dewell [2018] Fam CAFC 94:

‘Control is not sufficient of itself. What is required is control over a person or entity who by reason of the powers contained in the trust deed can obtain or effect the obtaining of a beneficial interest in the property in the trust.’

- Primary Beneficiary: while the husband was a primary beneficiary, this of itself created no legal title to the trust property

- Sham? There was nothing to suggest that the structure of dead Dad’s Will was a sham

- Sister had her own Divorce Protection Trust in her dead dad’s Will: that is fine. Having more than one Divorce Protection Trust in a Will is acceptable

- Good records: the court was impressed with the accountant for his excellent records, resolutions and tax returns. Each trustee was ‘scrupulous’ in filing separate tax returns, making resolutions under the trust deed and avoiding the mingling of trust assets. Professor Brett Davies stated

“rarely does the Court see a family law matter where tax returns and disclosure is so up-to-date and thorough.”

Was the Divorce Protection Trust merely for the benefit of the divorcing son?

Although this is not directly mentioned in the case, the Divorce Protection Trust is not for the sole benefit of the divorcing husband. It is not a ‘bare trust‘.

Instead, it is a trust that can benefit many generations. That is one of the four requirements that Legal Consolidated puts in your Divorce Protection Trust.

Does a Divorce Protection Trust work if there is only one child?

The 3-Generation Testamentary Trust Will states that the role of the Appointor is initially under the control of each Primary Beneficiary, as defined in the 3-Generation Testamentary Trust Will.

However, the Primary Beneficiary must have overcome four hurdles:

- reached the Age of Majority

- not be divorced

- not be bankrupt

- be of sound mind.

Having satisfied the hurdles, the Primary Beneficiary may establish as many testamentary trusts as they wish for their part of the estate. They can appoint trustees and appointors as they see fit (e.g. a brother, a company or themselves). If you have to narrow estate planning down to one word, it is ‘flexibility’. The 3-Generation Testamentary Trust Will is very flexible. Therefore, after you die, each primary beneficiary will plot and plan with their accountant, financial planner and lawyer to set up the trusts that best suit that purpose. In your Will, you gave them a lot of discretion; this is a great gift from you, the Will maker.

Should another child control the Divorce Protection Trust?

Q: I have two children. Is it better protection if, after I am dead, they are the Trustee or Appointor (Primary Beneficiary) of the other Testamentary Trusts? Do you recommend that each of the children be the trustee for the other’s Testamentary Trust?

And, should each of the children remain as Appointors of their own Testamentary Trusts?

For example:

- Bill is the Trustee of Sue’s Trust. Sue is the Appointor and Primary Beneficiary of this Trust.

- Sue is a Trustee of Bills Trust. Bill is the Appointor and Primary Beneficiary of this Trust.

I am aware of the case Bernard v Bernard. But I would like to get your practical perspective based on your Divorce Protection Trust. This is because Legal Consolidated’s Divorce Protection Trust goes one step further than the Testamentary Trust in Bernard’s case. It automatically removes the Primary Beneficiary’s power when attacked. This is very strategic.

A: The Divorce Protection Trust is designed to operate even if there is only one beneficiary in your Will. For example, your only child is Fred. When you and your spouse both die, Fred is the sole executor and the sole Primary Beneficiary. That is fine.

The wealth in your Will is left not just to Fred. But for 100s of other potential beneficiaries. The way Legal Consolidated drafts the Divorce Protection Trust is that Fred loses control if there is any activity or threat by his partner, spouse, or mistress. Another person, other than Fred, takes control. That may be Fred’s company, friend or relative.

But of course, the more you muddy the water, as they did in Bernard’s case, the harder it is for the divorce courts and bankruptcy courts to hand over your hard-earned money in your Will to your child’s divorcing partner. So mixing up the Trustee position is common. And the fictional Fred can do that by interposing a corporate trustee, a friend, or a relative to hold the trusteeship. The Legal Consolidated Divorce Protection Trust authorised and allowed that strategy. And Fred may well set it up that way after you are dead.

However, while the Divorce Protection Trust allows it – because it is full of flexibility – I find the strategy of having another person as the Appointor not to be the best. If you are the Appointor (or rather Primary Beneficiary, at the moment of death), then the Appointor controls the money.

When does the Divorce Protection Trust operate?

The Divorce Protection Trust sits dormant in the dead person’s Will until needed. The Divorce Protection Trust activates for the benefit of the married person and that person’s children and grandchildren. (This is your divorcing child, then their children and their grandchildren). The assets in the Divorce Protection Trust are provided by the parents (you), not the married person (e.g. your child). There is higher protection from the Family Court because of this. See, for example, Bernard v Bernard. The money is not from the divorcing couple. It is from an external person – the Will-Maker.

Your descendants (children, grandchildren and great-grandchildren) are beneficiaries of the Divorce Protection Trust but not owners of the assets.

What if a descendant controls the trust? This is where the descendant is the sole trustee or appointor. (This position of power controls the trust.) The Family Court states that the ‘controller’ is also the ‘owner’.

In these circumstances, a court may decide that it has the power to make an order affecting assets held by the trust. For example, the Court may order the transfer of the trust assets to the controller’s former spouse or to a trustee in bankruptcy.

However, the Divorce Protection Trust removes that person’s power to control the trust while they are suffering the separation. This removes control.

Who is the new Trustee of the Divorce Protection Trust?

The Primary Beneficiary under attack is automatically removed from all positions of power for their testamentary trusts. This includes the Appointor and Trustee positions. The power passes to the other executors named in the dead person’s Will, or to their next of kin if they are also dead, or, if there are none, to the blood relatives of the Primary Beneficiary. Of course, the Primary Beneficiary can always amend the Divorce Protection Trust to change this.

For example, widower Dad has 3 children. He leaves them everything and makes them the executors. Dad dies, leaving 33 1/3% of the assets to his son Gavin. Ten years after Dad dies, Gavin separates from his hot trophy wife. Immediately, his two other siblings are in control of all the testamentary trusts Gavin received from his Dad. However, one is dead, and their children take on the job. They must act only in the best interests of Gavin and his children. So the siblings and their children cannot benefit themselves from the trust.

The Divorce Protection Trust benefits current and succeeding generations. It protects your children, grandchildren and great-grandchildren for up to 80 years after you die. This helps keep your estate assets out of Family Court’s reach.

Why does the Family Court look at assets your child does not own?

The matrimonial pool includes:

- assets held in the parties’ individual or joint names

- businesses

- inheritances received in their personal names

- superannuation

- assets held within trust structures.

Financial resources typically include trust income or capital to which the parties have access.

Not all testamentary trusts protect against the Family Court’s powers. The Court has wide powers:

- power to make orders against the trustees of trusts

- power to make orders that direct or alter the rights, liabilities or property interests of a third party

- power to attribute a trust as a financial resource of a party to the marriage and adjust the matrimonial pool available for distribution accordingly.

Can a 23-day marriage still trigger the Family Court? Hsiao v Fazarri

Consider Hsiao v Fazarri [2020] HCA 35. The husband and the second wife began an intimate relationship before he separated from his first wife. Not ideal estate planning. Not ideal cardiac care either.

The relationship continued for years, but the parties lived in separate homes. The Court found that they did not start a de facto relationship. Then they married. The second marriage lasted 23 days.![Hsiao v Fazarri [2020] HCA 35 short relationships show that the Family Court will immediately consider a dead persons assets](https://legalconsolidated.com.au/wp-content/uploads/my-deceased-assets-are-lost-when-my-children-divorce.png)

The husband was wealthy. His assets were about $20m before his property settlement with his first wife. The young second wife had far fewer assets, but she had leverage. Romance does that. So does a hospital bed. The husband bought a Melbourne property. He first gave the second wife a 10% interest. Later, while in hospital with a suspected heart attack, he signed a transfer giving her a further 40%. That made them joint tenants.

After the 23-day marriage ended, the second wife wanted more. She argued about the property, the deed of gift and the extra 40% interest.

The second wife did not get the windfall she wanted. The Court ordered her to transfer her interest in the property back to the husband. She ended up with only $430,000. That sounds like a small result against a wealthy husband. But do not miss the point.

A 23-day marriage still opened the Family Court door. It still led to years of litigation. It still reached the High Court. It still put gifted property, joint tenancy, deeds of gift and relationship history under a microscope.

Similarly, if you die today, your children’s spouses have immediate access to your inheritance without a Divorce Protection Trust in the Will.

Does a Divorce Protection Trust in your Will protect your children BEFORE you die?

The Divorce Protection Trust protects your assets AFTER you die. It not only protects your children, grandchildren and great-grandchildren, but it also protects all beneficiaries and their offspring. It is not just for your children. The benefit is for all beneficiaries – whether related to you or not.

But, in this instance, your children (or beneficiaries) are divorcing, and you are still alive. Your Will does not operate until you die. And you can change your Will. But the Family Court can still consider the ‘potential’ gift. The Family Court, therefore, gives more money to the ex-in-law. This is on the basis that your child gets some money under your Will, at a later time when you are dead!

What is a Prospective inheritance?

A prospective inheritance is an anticipation of getting assets in the future. The Will maker may change their Will or go bankrupt. Therefore, the courts often exclude prospective inheritances from the divorcing couple’s property pool. But it may consider such ‘expectancies’ either as a financial resource (s 75(2)(b)) or as ‘any other matter that is relevant’ (s 75(2)(o)).

Prospective inheritances are not marital property. This is because they have not been received yet. They are also ‘mere expectancies’. However, the all-powerful Family Court can take into account prospective inheritances. Consider the cases below: White & Tulloch and de Angelis v de Angelis.

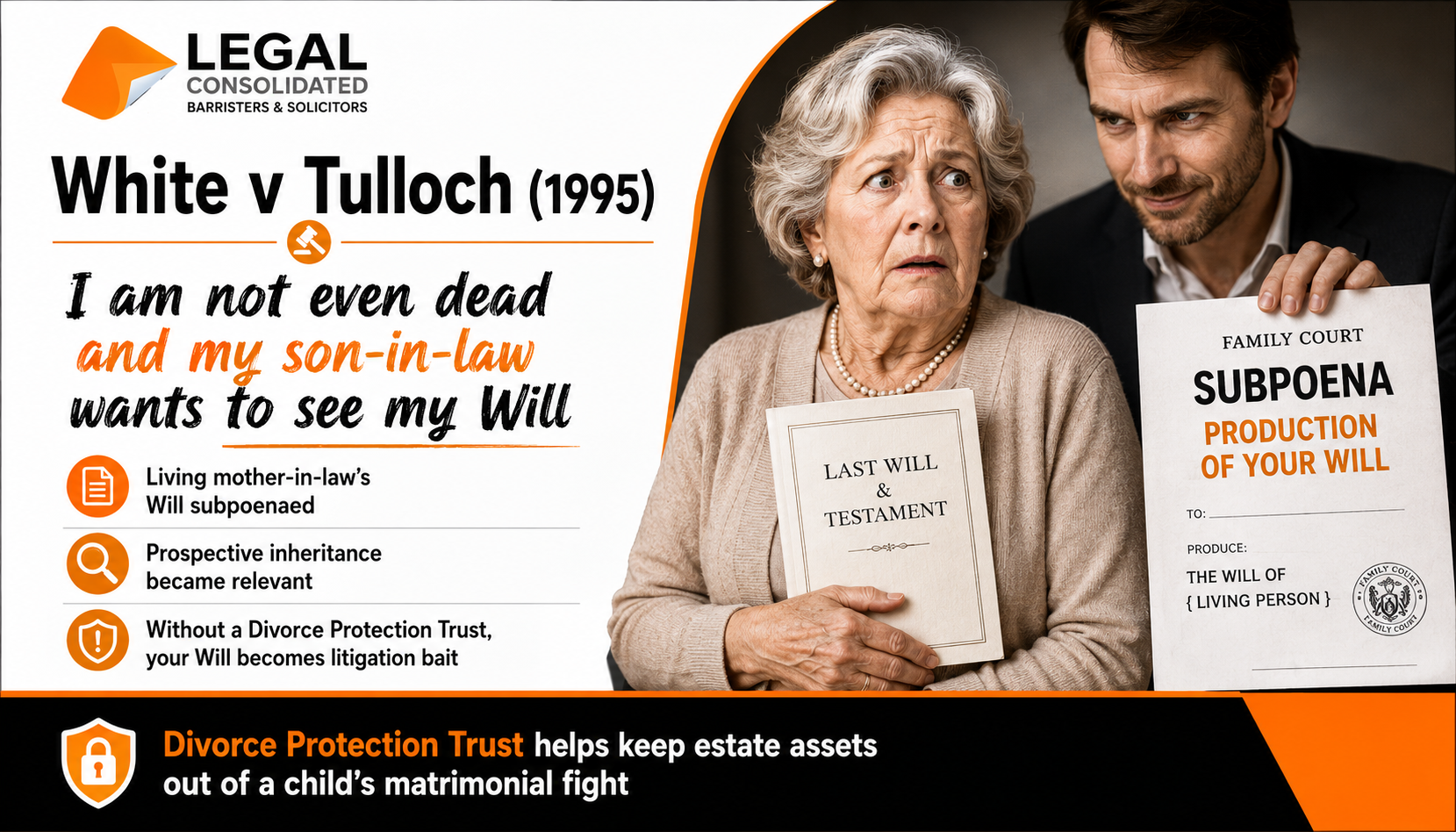

The Family Court looks at your Will before you die: White v Tulloch

In Hsiao v Fazarri (above), a 23-day marriage was enough to open the door to the Family Court. White v Tulloch (1995) 19 Fam LR 696 goes further.

In this case, the Will-maker is not yet dead.

Poor old mum made a Will. At 81, she was in reasonable health. She had two children. Her Will left a likely inheritance to her daughter: the divorcing wife.

Mum’s son-in-law wanted to know what the wife may inherit. So he went after the mother-in-law’s Will.

The Family Court allowed the subpoena for the Will. Think about that. The mother-in-law was alive. Her Will had not taken effect. She could still die years later. She could still change her Will as she had the mental capacity. But the Will still became part of the Family Court fight.

That is the estate planning warning.

A possible inheritance is a financial resource. It becomes relevant if there is a worthwhile connection between the expected inheritance and the claims in the Family Court.

The Court said:

“There must be a worthwhile connection between a specific element of the party’s case and the suggested expectancy.”

That is enough to make any parent nervous.

You may think your Will is private until you die. Not always. In a child’s divorce, your Will may become evidence. Your estate planning may be dragged into your child’s matrimonial dispute before you are even dead.

What do we learn from White v Tulloch?

A direct gift in your Will is an easy target.

It tells the Family Court:

“Here is the child. Here is the inheritance. Here is the expected money.”

That is why a non-tax-effective Will is dangerous for wealthy parents. It gives no protective machinery. It just hands the inheritance straight to the in-laws. Once the child owns it, the spouse sees it. The Family Court sees it. The fight begins.

A Divorce Protection Trust in a 3-Generation Testamentary Trust Will gives the family protection. It keeps your estate assets out of your child’s exposed personal name and away from a spouse’s Family Court attack. Stop your Will from being litigation bait with a Divorce Protection Trust.

De Angelis states the same.

Dementia, a frozen Will and the Family Court: In the Marriage of De Angelis

In White v Tulloch, the Family Court looked at a living mother-in-law’s Will. That was bad enough. In the Marriage of De Angelis [1999] FamCA 1609; (2003) FLC 93-133 goes further. The expected inheritance was closer. Harder to dismiss. More dangerous.

The wife expected to inherit from her mother and her aunt. The likely inheritance included two properties. The aunt was about 90. She had dementia. She lacked the capacity to change her Will.

That matters.

A mentally healthy Will maker can update their Will. They can sell the house. They can spend the money. They can leave everything to the cat home. Until death, an inheritance is usually only an expectancy.

But when the Will maker has lost testamentary capacity, the Will is frozen. The Family Court looks harder. The child’s expected inheritance starts to look less like a vague hope and more like a future cheque.

The Full Court said there is “no absolute rule”. Each case depends on its own facts. But the Court asked whether it would be just and equitable to ignore the probability that, in what could be a very short time, the wife could own two properties worth almost as much as the existing matrimonial property.

Your child’s spouse does not need you to be dead before your estate planning becomes a target. If your Will lacks a Divorce Protection Trust, it is fixed, or you have lost testamentary capacity, the Family Court treats the expected inheritance as relevant.

What does De Angelis teach about Divorce Protection Trusts?

A simple Will leaves a clear trail:

“My child gets my estate.”

That is litigation bait. It tells the Family Court where the money is going. It tells the child’s spouse what to chase. It gives the court a clean story: the inheritance is coming, the Will maker cannot change the Will, and the child is likely to receive the asset.

A Divorce Protection Trust in a 3-Generation Testamentary Trust Will gives your family better machinery. It helps keep estate assets out of your child’s exposed personal name. It creates control levers. It makes the inheritance harder to describe as a simple cheque waiting for your child.

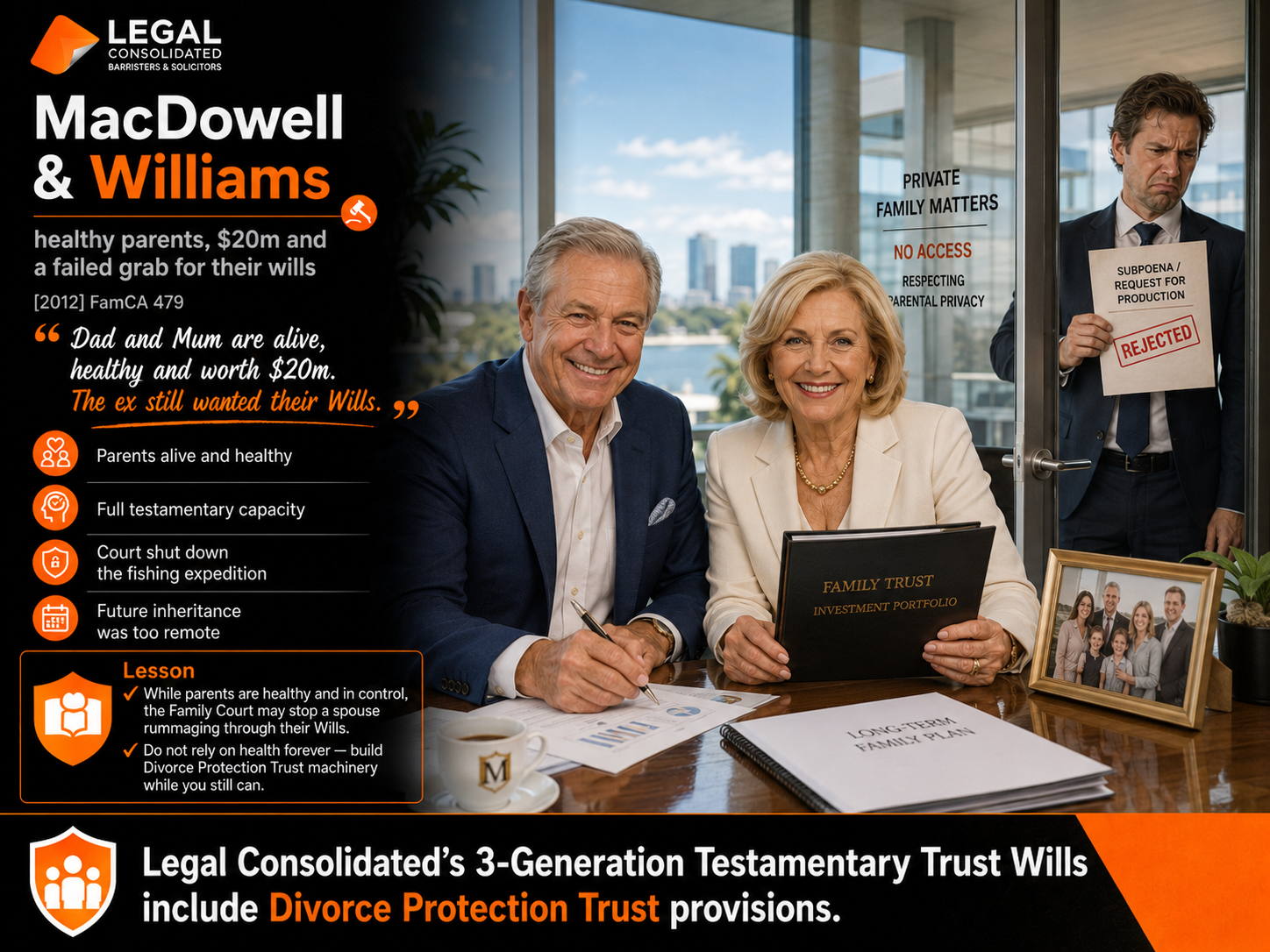

Healthy parents, $20m and a failed grab for their Wills: MacDowell & Williams

Sometimes the Family Court looks at a future inheritance. Sometimes it refuses. MacDowell & Williams and Ors [2012] FamCA 479 is the other side of White v Tulloch and In the Marriage of De Angelis.

In MacDowell, the husband wanted the wife’s parents’ Wills. He also wanted documents about their companies and trusts. Why? Because he said the wife may one day inherit part of an estate worth more than $20m. The parents objected.

They were alive. They had testamentary capacity. There was no evidence they were in poor health. They were aged 77 and 75. They were still running their investment business. They could change their Wills. They could leave everything to each other. They could spend the money. They could restructure their affairs.

Therefore, the Court refused to hand over their Wills. It treated the husband’s attempt as a fishing expedition. That is the practical lesson. A future inheritance is not automatically property. It is not automatically a financial resource. It is often just an expectancy.

But do not relax.

The Court contrasted this case with harder cases, such as those in which the Will maker has already lost testamentary capacity, is close to death, and has made a Will favourable to the divorcing child. In those cases, the Family Court may look harder.

The MacDowell & Williams Court quoted White v Tulloch:

“There must be a worthwhile connection between a specific element of a party’s case and the suggested expectancy.”

That is the line. If the connection is weak, the Court may refuse. If the connection is strong, your Will becomes evidence.

What does MacDowell teach about Divorce Protection Trusts?

MacDowell gives comfort, but only up to a point. If parents are alive, healthy, still have capacity and still control their own wealth, the Family Court may refuse to let a child’s spouse rummage through their Wills. But that protection is fragile.

Health changes. Capacity disappears. Death approaches. A Will becomes harder to change. A future inheritance can start to look less like a hope and more like a cheque waiting to clear. That is when a bare gift in a Will becomes litigation bait.

A 3-Generation Testamentary Trust Will with Divorce Protection Trust machinery provides greater protection. It gives your family control levers. It helps keep estate assets out of your child’s exposed personal name. It gives the family something to point to other than a direct gift waiting for the child. Do not rely on being healthy forever. Build the protective machinery while you still can.

What does setting up a trust to protect divorcing beneficiaries in my Will cost?

Legal Consolidated’s 3-Generation Testamentary Trust Wills always contain Divorce Protection Trusts as part of their arsenal of weapons to protect your beneficiaries. They are included in the cost of the 3-Generation Testamentary Trust Wills. There is no additional cost.

After you are dead, each beneficiary can turn ‘on and off’ many different trusts in your Will. This is as each beneficiary sees fit. For example, one beneficiary may set up four 3-Generation Testamentary Trusts to reduce capital gains tax on the sale of different properties in different states. Another beneficiary may ‘turn on’ the Bankruptcy Trust. The third beneficiary named in your Will may set up a Divorce Protection Trust for their percentage of your estate.

There is no cost to set up any of the trusts. The terms of the trust are contained in the 3-Generation Testamentary Trust. It is free to start any of the trusts. This is as each beneficiary sees fit.

What does it cost for my beneficiary to maintain a Divorce Protection Trust?

Like a Family Trust, a Testamentary Trust often needs to lodge a trust tax return. This is each financial year. This is with the Australian Tax Office.

Legal Consolidated is a law firm. We do not prepare tax returns, so you are better off approaching the accountant about the cost of lodging a trust return each year. We spoke to some accountants about what they charge. The accounting fees appear to be about $880 to $1,200 annually. But again, each accountant will charge differently based on the work involved. You are best to speak with your accountant.

Do I have to die before my children can use the Divorce Protection Trust?

Everything in a Will is dormant, that is, until the Will maker dies. The Divorce Protection Trust sits in the Will. Therefore, the Divorce Protection Trust does not operate before the Will maker’s death.

The Will is nothing but an expectancy. Indeed, the Will maker may make a new Will, leaving you nothing.

Both the Will and everything contained within it, including the Divorce Protection Trust, remain dormant. This is until the ultimate sacrifice is made — you die.

Only upon the Will maker’s death does the Divorce Protection Trust become able to be activated. So, while it might not be the most convenient requirement, you do have to die before your children can utilise the Divorce Protection Trust to safeguard the assets you give them in your Will against the potential complications of divorce and relationship breakdowns.

Protects from death duties, divorcing and bankrupt children and a 32% tax on super.

Build online with free lifetime updates:

includes 3-Generation Testamentary Trust Wills and 4 POAs

includes 3-Generation Testamentary Trust Will and 2 POAs

Death Taxes

Vulnerable children and spendthrifts

Second Marriages & Challenging Will

What if I:

Assets not in your Will

Power of Attorney

Money POAs: NSW, VIC, QLD, WA, SA, TAS, ACT & NT

Money POAs: NSW, VIC, QLD, WA, SA, TAS, ACT & NT

- Medical, Lifestyle, Guardianships, and Care Directives:

- Company POA when directors go missing, insane or die

After death